Most European rollout plans treat Romania as a line item near the bottom. Launch Germany, add France, maybe Italy or Poland, then plug Romania into a pan-EU warehouse once the rest is running. That sequence made sense when Romania was a thin, cash-only market with patchy delivery. It describes a country that no longer exists.

The Romanian ecommerce market closed 2024 at €11.7 billion in total turnover, with €7.7 billion of that spent on physical goods delivered by courier. Online sales now make up roughly 11% of total retail, and the market has posted double-digit growth for years while most of Western Europe settled into single digits. Romania also runs on habits that look strange from a Northern European desk. Cash on delivery still moves close to half of all orders. A single domestic group, eMAG, anchors the largest marketplace, a leading courier, and the dominant locker network at the same time.

This guide is the practical view for any brand weighing a 2026 entry: market size, who really buys, the payments to design for, and the logistics that decide whether a cross-border launch clears margin or eats it.

Romanian Ecommerce Market: Size and Growth Heading into 2026

How big is the Romanian ecommerce market really?

This is where sources disagree, and the disagreement changes your planning numbers. Anchor on GPeC. The Gala Premiilor eCommerce report, produced with the local merchants’ association ARMO, is the figure Romanian trade press quotes and the one industry leaders cite on stage. GPeC put 2024 at €11.7 billion in total ecommerce turnover, up about 10% year on year, of which €7.7 billion went to physical, courier-delivered products. The rest is services: travel, tickets, utilities, digital subscriptions.

For a brand shipping boxes to Romanian doorsteps, the €7.7 billion product figure is the one to plan against, not the headline. The gap between the two is exactly the kind of thing that quietly inflates a market-size slide and then disappoints a launch.

| Source | Headline figure (latest) | Scope | Best used for |

| GPeC / ARMO | €11.7B total in 2024 (€7.7B physical goods) | Total turnover, goods + services | The headline local press uses |

| Mordor Intelligence | ~11.6% projected CAGR; B2C ≈ 84% of value | B2C market size + forecast | Forward-looking B2C planning |

| ecommerceDB / Statista | Physical-goods B2C net sales (narrower) | B2C physical goods only | Retail-only benchmarking |

The methodologies measure different things, so the absolute numbers never line up. They agree on direction: Mordor Intelligence models the Romania ecommerce market growing at roughly 11.6% a year over the next five years, with B2C holding around 84% of value.

Pace, trajectory, and the Central and Eastern Europe context

Romania is the fast lane of Central and Eastern Europe right now. The market grew about 10% in 2024 and players model another 10% or more for 2025, driven by boring fundamentals: late maturity catching up, near-universal internet penetration, and a delivery network that finally reaches the villages. GPeC’s founder Andrei Radu frames the 11% online share of retail as the opportunity, not the achievement. Plenty of runway left.

Against the rest of the region, Romania sits behind Poland in absolute size but ahead on momentum. It is one of Europe’s most underbuilt large markets and one of its fastest-improving. The same gap that opened up in the Spanish ecommerce market and the Italian ecommerce market, where cross-border sellers underrated Southern Europe for years, is opening in Romania now. Eurostat data shows Romania still has one of the lowest shares of online shoppers in the EU, alongside Italy and Bulgaria, yet it also gives Romania the biggest ten-year jump in e-shopper share of any member state, up 46 percentage points between 2015 and 2025. Low base, steep curve.

Key Point: A low online share is the opportunity, not the warning. Romania is moving from “some people discover online shopping” to “most people shop online by default,” and that is the phase where fulfillment quality, locker coverage, and payment fit start deciding who wins. The brands that build for the market Romania is becoming, not the one it was in 2019, get the easy years.

Who Shops Online in Romania?

Romania had 17.8 million internet users at the start of 2025, an internet penetration rate near 94% of the population. Around 60% of those internet users placed an online order in 2024, up from a meager 17% a decade earlier. The growth is no longer coming from young, urban early adopters; they crossed that line years ago. It is coming from older shoppers and from rural areas, where faster courier coverage, cheap mobile data, and automated pickup points removed the friction that used to keep people offline.

That rural swing is the demographic story of the last two years. ARMO’s executive director, Cristian Pelivan, ties it to expanding courier routes and high-speed internet reaching small towns. Urban internet users still shop online at a higher rate than rural ones, around three-quarters versus seven in ten on Eurostat-based 2025 data, but the rural figure is the one climbing fastest.

Bucharest, the cities, and the rural surge

Order density is concentrated, and Bucharest sits at the center of it. The capital and its surrounding Ilfov County generate a disproportionate share of both supply and demand: most merchants, marketplaces, and logistics hubs cluster there, and most parcels land there too. Cluj-Napoca, Timișoara, Iași, Brașov, and Constanța form the second tier and behave like Bucharest on conversion and delivery time.

Beyond the cities, the map stretches. Rural Romania and the mountainous interior run longer last-mile times and higher per-parcel costs, though the gap narrows as locker grids push into county seats. A Bucharest-anchored operation serves most of the value quickly, and the rural surge is best reached through automated pickup points rather than expensive home-delivery attempts.

Features of the Romanian Ecommerce Market

Mobile owns the checkout

Romania is a mobile-first market even by European standards. Romanian online shoppers reach for a smartphone more than almost anyone else on the continent, and recent sector data puts the smartphone share of ecommerce transactions in the low-to-mid 70s. Mordor Intelligence estimates smartphones accounted for about 74% of the Romania ecommerce market by transaction in 2024.

A checkout that needs a desktop or two thumbs of typing leaks conversion here. One-tap payment, biometric login, and a basket that survives a single-handed scroll are the floor. Product discovery happens on the phone too, often inside a marketplace app or a social feed.

Domestic champions own the value

Here is the feature that surprises sellers who only know Western Europe. Romanians buy cross-border often, but a large share of the money stays home. More than half of Romanian online shoppers bought from foreign websites at least twice in 2023, a rate above the European average, and global platforms like Shein, Temu, and AliExpress pull serious volume in fashion and low-cost goods. The Turkish marketplace Trendyol opened a logistics center near Bucharest built to handle at least 2.5 million deliveries a year. Cross-border payment volume jumped sharply through 2024.

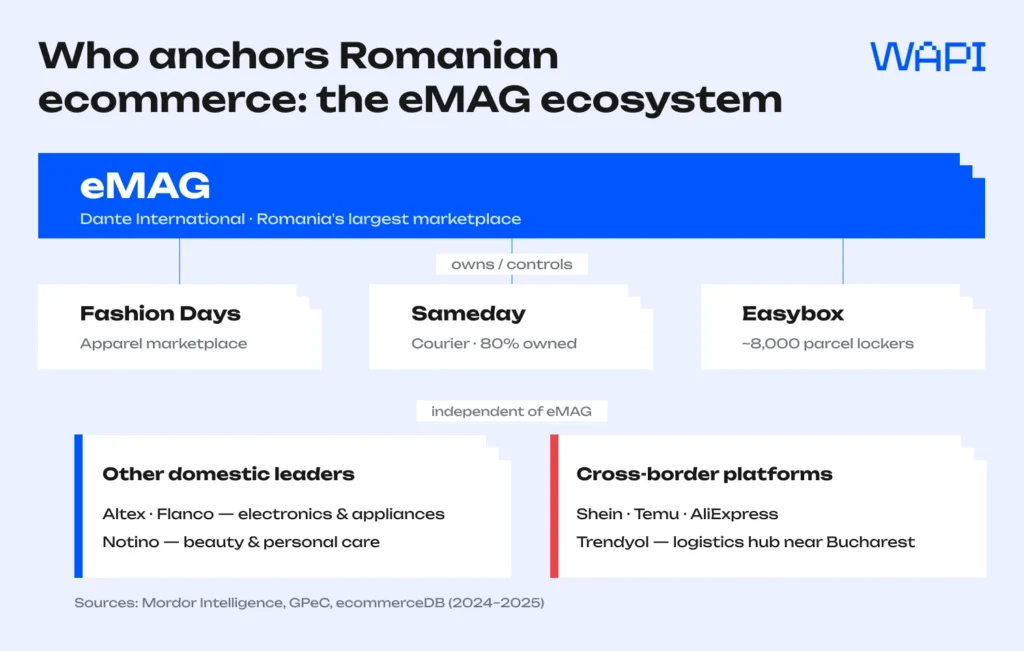

And yet, by value, Romania leans more domestic than Spain or even Italy. The reason is one company. eMAG, run by Dante International, dominates the local landscape the way Allegro dominates Poland, and it owns the pieces around it: Fashion Days for apparel, an 80% stake in the Sameday courier, and the easybox locker network that rides on top. eMAG grew about 14% in Romania in 2024 and, on Mordor Intelligence’s figures, posted Romanian sales of roughly RON 7.7 billion (about €1.5 billion) that year, with tens of thousands of third-party merchants on its marketplace. Altex Romania SRL and Flanco hold the electronics and appliance lanes, with Notino strong in beauty. Foreign brands are not facing a fragmented field of small shops; they face a vertically integrated home-team ecosystem that controls discovery, delivery, and the locker your customer walks to.

That cuts two ways. The barrier to the top is real, but the same infrastructure is rentable. You can sell through eMAG and Fashion Days for reach, ship through Sameday and FAN Courier for speed, and still run your own store for margin. Romania also works as an export base: eMAG has pushed into Hungary and Bulgaria, and Romania’s position makes it a natural launchpad into the wider Central and Eastern Europe region.

Top product categories

Two categories carry the Romania ecommerce market, and which one leads depends on whose definition you use.

- Consumer electronics and IT — the historical engine, owned by eMAG, Altex Romania SRL, Flanco, and Media Galaxy. High average order values, heavy warranty and returns handling, and a Black Friday peak Romania treats as a national sport, so the fulfillment job is serial-number tracking, secure packaging, and surge capacity.

- Fashion and apparel — close to the top and the biggest category by some measures, with Mordor Intelligence putting it near 31% of 2025 B2C revenue. Fashion Days, Shein, and Zara anchor it. The pain is return rates: size exchanges and try-before-keep behavior make a local return address non-negotiable.

- Beauty and personal care — a strong cross-border pull led by Notino and dm and driven by influencer spikes. Fragile packaging, batch and lot tracking, and the ability to absorb a sudden campaign-driven order surge separate the operators from the amateurs.

- Food and grocery — slower but accelerating through quick-commerce apps and Wolt’s takeover of the local Tazz service. Mostly local and temperature-sensitive, so it sits outside standard parcel fulfillment.

- Supplements and specialized goods — smaller, but the place where handling beats price. Expiry-date and batch traceability plus regulated-product documentation turn into a real edge past a few hundred parcels a week, which is where category-specific supplement fulfillment stops being overhead and becomes a moat.

What Romanian Consumers Expect

Romanian buyers are pragmatic. They do not need theatrical promises; they need proof you will deliver what the photo showed. Surveys of what drives store choice put free delivery on top, cited by roughly a third of shoppers, followed by clear product descriptions, the option to pay cash on delivery, and free returns. Hidden costs that surface on the final screen kill conversion the same way they do everywhere else.

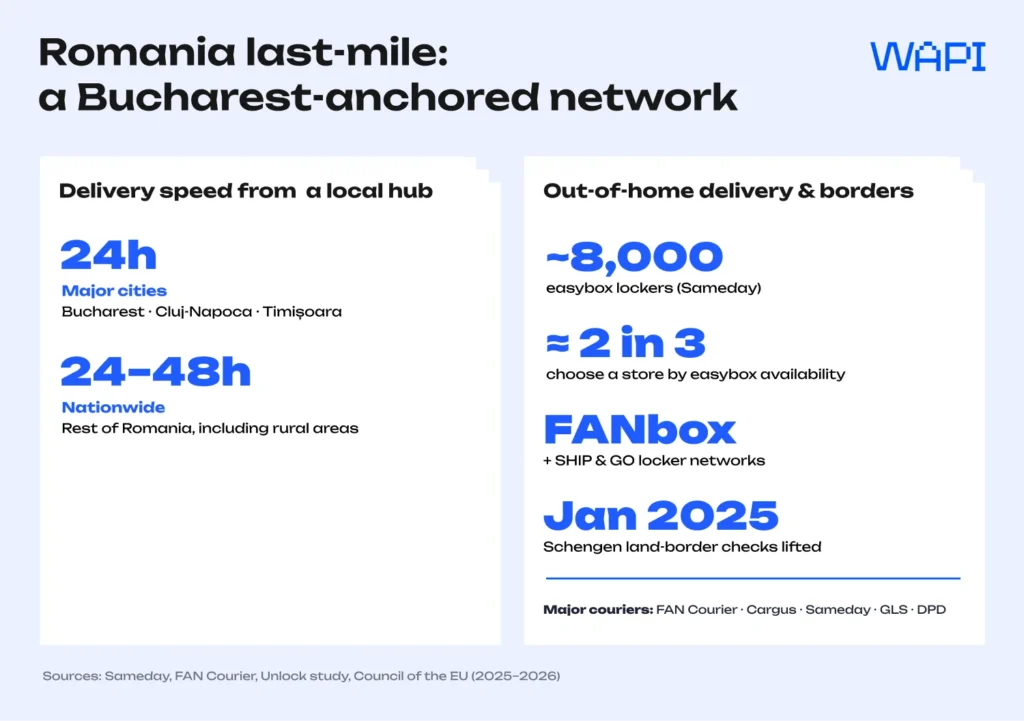

Out-of-home delivery moved from niche to default faster in Romania than almost anywhere in Europe, and lockers led the shift. An Unlock study found that about two-thirds of Romanian consumers pick an online store partly based on whether easybox delivery is offered. The networks worth integrating at checkout:

- easybox (Sameday) — the giant, with around 8,000 easybox lockers across Romania and Bulgaria and tens of millions of parcels routed through it. eMAG’s ownership wired it straight into the country’s biggest marketplace.

- FANbox (FAN Courier) — the locker arm of Romania’s most widely used courier, expanding nationally.

- SHIP & GO (Cargus) — Cargus’ out-of-home delivery network, subject to ownership changes under the Sameday–Cargus remedies.

- Same-day in major hubs — available in Bucharest, Cluj, Timișoara, and other large cities through eMAG, quick-commerce apps, and grocery players.

Our advice: Don’t try to win the basket by burying the shipping cost or over-promising same-day across the whole country. Romanian shoppers want the delivery option they already trust, which is increasingly a locker near home or work, and they want the price honest from the start. A reliable final-mile delivery partner that hits its tracking events beats an aggressive cutoff that slips. Predictability wins repeat customers; heroics win one order and a support ticket.

Returns are the quieter margin question. Fashion rates run high enough that, without a local return address, you either eat the inbound shipping or push it onto the customer and lose the sale. A domestic returns flow is the line between a viable Romanian P&L and a leaky one.

Payment Methods Romanian Customers Actually Use

Read the Romanian payment mix as a set of source-dependent signals, not a clean split. Different studies count different things, and cash on delivery is where they diverge most.

| Method | Approx. share / signal | Notable players | Trend |

| Cash on delivery | ~51% of orders (2025 peak-season data); higher in some merchant datasets | FAN Courier, Sameday, Cargus, DPD | Declining slowly |

| Cards (debit + credit) | ~45% of value | Visa, Mastercard, Netopia, PayU | Stable, slowly declining |

| Digital wallets | ~10% of transactions, plus marketplace wallets | Google Pay, Apple Pay, PayPal, eMAG Wallet | Growing fast |

| BNPL / installments | ~7%, up over 100% in 2024 | TBI Bank, eMAG HeyBlu, PayU instalments | Strong growth |

| Bank transfer / A2A | smaller, higher-ticket | SEPA, internet banking | Stable |

A few methodology notes before the advice. The COD figure swings by study: one peak-season read put it around 51% of orders, some merchant datasets push the share of payment value higher, and a 2023 survey found roughly 21% of shoppers name cash on delivery as a reason they choose a store. They measure orders, value, and motivation, which are three different things. The honest summary: cash on delivery still accounts for something close to half of Romanian online orders, one of the highest rates in the EU, and it is sliding gently rather than collapsing. Card payments anchor the cities and repeat buyers, and on PayU’s data digital wallets are the fastest-climbing modern rail while BNPL more than doubled in 2024.

Cash on delivery still rules, and what to do about it

If Bizum is the Spanish payment story, cash on delivery is the Romanian one. It exists for reasons that have not gone away: distrust of paying before seeing the product, thinner card adoption in rural areas, and the simple comfort of handing money to a courier. Many shoppers also use COD as an informal inspection right, refusing at the door if the box looks wrong.

For a seller, COD cuts both ways. It lifts conversion with cautious, first-time, rural, and older buyers, and stays close to mandatory for reaching them. It also locks inventory in transit, raises the cost of refusals, and demands a partner who can collect and reconcile the cash cleanly.

Insight: Treat cash on delivery as a conversion lever you manage, not a liability you tolerate. Offer it everywhere, but pair it with thresholds on high-value orders, confirmation on risky baskets, and small nudges toward card or wallet payment over time. A logistics partner that handles cash on delivery end to end, with collection, reconciliation, and real-time signals on failed or refused deliveries, turns Romania’s cash habit from a margin drag into a reason customers click buy. The same setup carries across the rest of Central and Eastern Europe, where COD is still a leading method.

Romanian Logistics Realities

Romania’s last mile is better and cheaper than its reputation suggests, at least along the Bucharest-Cluj-Timișoara-Iași corridor, where Sameday, FAN Courier, Cargus, GLS, and DPD compete hard. Romania’s full Schengen accession from January 2025 removed internal land-border checks on persons and improved the broader cross-border environment, though parcel performance still depends on linehaul, carrier handoffs, and returns processing rather than customs.

The economics still flip toward local inventory once volume is real. Shipping into Romania from a German or Polish warehouse stacks transit time and handling onto every order, the very margin that justified going cross-border in the first place.

The easybox effect and last-mile consolidation

The locker boom reshaped Romanian delivery faster than anyone forecast. easybox, FANbox, and SHIP & GO between them now cover the suburbs of every metro and most secondary cities, and consumers stopped treating a locker as a downgrade years ago. Lockers cut failed first-attempt deliveries, lower per-parcel cost, and match how mobile-first Romanians already behave.

The market is also consolidating in plain sight. Sameday’s acquisition of Cargus, the first private courier founded in Romania, was announced in 2025 and conditionally approved by Romania’s Competition Council in April 2026, pushing the courier market toward deeper consolidation. For a seller, that points to fewer, deeper carrier integrations over time and even more gravity around the eMAG ecosystem. Plugging into the dominant locker networks at checkout typically lifts completed orders and trims redelivery costs.

What to Set Up Before Shipping to Romania

Before launching or scaling into the Romania ecommerce market, have these five blocks in place:

- Carrier mix — at least one home-delivery courier plus locker integration via easybox, FANbox, and Cargus SHIP & GO. Single-carrier setups underperform, and lockers are where Romanian demand is moving.

- Payment setup — cash on delivery is close to non-negotiable, paired with cards, digital wallets, and BNPL for relevant categories. A COD operation you can reconcile cleanly matters as much as the checkout itself.

- Returns setup — a local or regional return address, fast inspection, and inventory recirculation. Without it, fashion and beauty break above modest volumes.

- Compliance — Romanian VAT handling, the mandatory RO e-Factura electronic invoicing for VAT-liable activity, Romanian-language product and label checks, and batch traceability for supplements and cosmetics.

- Category specifics — fashion returns workflows, cosmetics handling with batch tracking and restricted-shipping rules, and supplement documentation for the competent Romanian authority.

Skip these and the failure mode is predictable: returns pile up at a foreign warehouse, conversion slides on a checkout missing COD, and support tickets stack up over delivery transparency. None of it shows up in a market-sizing report, which is exactly why it ambushes teams six months in.

How Cross-Border Sellers Should Approach the Romanian Market

Local fulfillment beats pan-EU once volume is real

For a low-volume test, a German or Polish warehouse handles Romania fine. Past a few hundred parcels a week, the math tilts toward a dedicated fulfillment center in Romania: faster delivery, lower last-mile cost, a domestic returns address, and clean COD collection that a remote setup cannot match.

The arithmetic is blunt. A €3 saving per parcel on 500 parcels a week is roughly €78,000 a year, enough to fund the local switch and still come out ahead. The question for most cross-border brands is not whether to set up ecommerce fulfillment in Romania, but when.

Five signs it’s time to set up Romania fulfillment:

- Romanian order volume holds at 300+ parcels per week for two consecutive months.

- Return rate clears 25%, especially in fashion or beauty.

- Support tickets spike on transit-time and tracking complaints.

- Paid acquisition efficiency drops because conversion is bottlenecked on the delivery and payment promise.

- COD reconciliation and refused-delivery costs from a remote setup start visibly eroding margin per order.

Localize beyond translation, layer marketplaces with DTC

Romanian-language product pages, Romanian customer support, and Romanian-language return instructions are table stakes. Real localization means pricing in lei with VAT shown, offering cash on delivery and lockers as first-class options, and pacing delivery promises against eMAG, not against your home market. A translated template on top of an English store does not count as a market entry.

eMAG, Fashion Days, Altex, and Flanco dominate Romanian online traffic, so the resilient play layers them on top of a localized store. Sell through the marketplaces for discovery and trust, and run your own ecommerce fulfillment and DTC site for margin and customer data. Marketplace-only exposes you to fee and algorithm shifts; DTC-only means slow, expensive acquisition where the marketplaces hold the audience. The hybrid model is the safer play: marketplaces for reach, DTC for margin and customer data.

Final Take: Romania Rewards Operators, Not Tourists

The Romania ecommerce market has quietly become the most interesting growth story in Central and Eastern Europe: double-digit growth, an internet base near 94%, a rural surge adding the most new buyers, and a locker network that already rivals Western European density. It also has sharp edges, from cash on delivery to a domestic ecosystem you work with rather than around. Those are operator problems, not marketing problems.

Our advice: Treat Romania as a logistics-and-payments market, not a translation exercise. The brands that win in 2026 match their fulfillment, COD handling, locker coverage, and returns to the bar eMAG set. Build for how Romania really buys, and the growth curve does the rest.

FAQ

How big is the Romanian ecommerce market?

Romanian ecommerce reached €11.7 billion in total turnover in 2024, up about 10% year on year, with €7.7 billion of that spent on physical goods delivered by courier (GPeC / ARMO). Online sales make up roughly 11% of total Romanian retail, which leaves significant room to grow. Research houses like Mordor Intelligence model continued double-digit growth, around 11.6% a year, over the next five years.

Is Romania a good market for cross-border ecommerce?

Yes, with a caveat. The market grows at double the Western European rate, internet penetration is near 94%, and rural adoption is climbing fast. The catch is that domestic players, led by the eMAG ecosystem, hold much of the value, and consumers expect cash on delivery and locker pickup. Sellers who localize payments and logistics do well; sellers who treat Romania as a translated version of Germany struggle.

What is the most popular payment method in Romania?

Cash on delivery remains the defining method, accounting for roughly half of online orders, one of the highest rates in the EU. Card payments anchor the cities and repeat buyers at around 45% of value, digital wallets like Google Pay, Apple Pay, and the eMAG Wallet are the fastest-growing rails, and BNPL more than doubled in 2024. A checkout for Romania should offer COD, cards, and a wallet at minimum.

Do Romanians prefer lockers or home delivery?

Both, but lockers grew explosively and are now a primary expectation. Around two-thirds of Romanian consumers say easybox availability influences which store they buy from. Sameday’s easybox network alone is around 8,000 lockers, with FAN Courier’s FANbox and Cargus SHIP & GO adding coverage. Offering locker delivery at checkout lifts completed orders and cuts redelivery costs.

Do I need a Romanian company to sell ecommerce in Romania?

Not for most cross-border setups. EU sellers can ship into Romania under the One-Stop Shop (OSS) VAT scheme from their home country, and non-EU sellers can use IOSS for consumer parcels under €150. A local entity helps if you hire in Romania, open a local bank account, or run paid acquisition with Romanian billing, but it is rarely required upfront. VAT-liable activity does need to comply with the mandatory RO e-Factura electronic invoicing system.

What are the biggest online stores in Romania?

eMAG (Dante International) is the dominant marketplace, comparable to Allegro in Poland, and it owns Fashion Days in apparel plus a controlling stake in the Sameday courier. Altex Romania SRL and Flanco lead consumer electronics and appliances, Notino is strong in beauty, and global platforms Shein, Temu, AliExpress, and the newly arrived Trendyol pull cross-border volume. Together, eMAG, Fashion Days, and Altex account for a large slice of total Romanian ecommerce revenue.

Does WAPI have a warehouse in Romania, and how fast is delivery?

Yes. WAPI runs warehousing and fulfillment in Romania positioned on the country’s key transport corridor. Orders reach major cities like Bucharest, Cluj-Napoca, and Timișoara within 24 hours, nationwide within 24 to 48 hours, and most EU destinations in 2 to 3 days. The Romanian hub also opens fast access to nearby markets like Bulgaria and Hungary.

Does WAPI offer cash on delivery in Romania?

Yes. Cash on delivery is one of WAPI’s core services, which fits Romania well given how much of the market still pays at the door. WAPI handles COD end to end, including collection, reconciliation, and signals on trouble statuses like failed or refused deliveries, so the cash habit becomes a conversion lever rather than an operational headache. The same COD capability extends across WAPI’s wider European network.

What can WAPI store and handle in its Romanian warehouse?

WAPI’s Romanian warehouse handles supplements, cosmetics, electronics, and general consumer goods, with dedicated storage and packing for supplements and cosmetics, though not perishable food. Value-added services include labeling, fragile-item packaging, kitting and assembly, quality-control inspection, repackaging, and returns processing, all tracked through WAPI’s warehouse management system with real-time inventory visibility and out-of-the-box integration with Shopify, eBay, BigCommerce, and Amazon.

Sources and References

- GPeC / ARMO — E-Commerce Romania 2024 report (presented at ZF eCommerce Summit 2025): €11.7B total market, €7.7B physical goods, +10% YoY, 11% of retail online — gpec.ro

- DataReportal — Digital 2025: Romania: 17.8M internet users, 94% internet penetration, 25.3M mobile connections — datareportal.com

- Eurostat — E-commerce statistics for individuals (2025): e-shopper share and +46pp ten-year growth — ec.europa.eu/eurostat

- Mordor Intelligence — Romania E-commerce Market: ~11.6% CAGR, B2C ≈ 84% of value, smartphone ≈ 74% of transactions, cards ≈ 45% of value, fashion ≈ 31% of B2C revenue, key players — mordorintelligence.com

- PayU GPO / The Paypers — Romania 2025 payments & ecommerce trends: digital wallets ≈ 10% of transactions, BNPL +100% YoY — thepaypers.com

- Business Review / Ecommerce Germany — Romania payments overview (2025): cash on delivery ≈ 51% of orders — ecommercegermany.com

- Sameday / OrderTracker / Competition Council — easybox & Cargus: around 8,000 easybox lockers; Cargus acquisition announced 2025, conditionally approved by Romania’s Competition Council on April 2, 2026 (locker divestiture and customer-terms remedies), pending finalization — sameday.ro, consiliulconcurentei.ro

- Romania Insider / Ecommerce News Europe: cross-border share (54% in 2023), Trendyol logistics center, eMAG +14% growth — romania-insider.com, ecommercenews.eu

- ecommerceDB / Statista: leading Romanian online stores (eMAG, Fashion Days, Altex) — ecdb.com

- WAPI — Warehouses in Romania: service details, delivery times, courier network, value-added services — wapi.com/warehouses-romania

Keep in touch with WAPI!

Get free ecommerce tips, news, webinars and other stuff.