Italy is the EU’s third-largest economy and one of Europe’s most important consumer markets, yet many cross-border sellers still treat it as a secondary target — too fragmented, too cash-loving, too logistically complex.

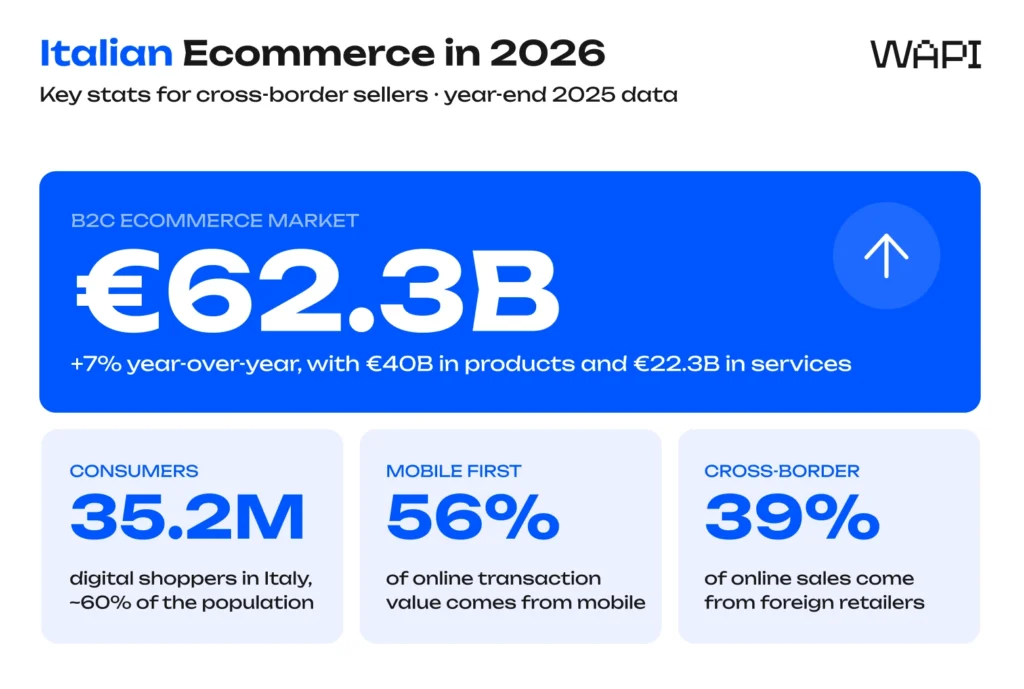

The picture entering 2026 is different. Italian B2C ecommerce closed 2025 at over €62 billion in transactions, mobile drives more than half of all online spending, and digital wallets have overtaken cards at checkout.

This guide breaks down what foreign brands actually need to know to operate in Italy in 2026 — the size, the consumers, the payment habits, and the logistics realities that quietly decide whether a cross-border launch turns profitable.

Italy Ecommerce Market: Size and Growth Heading into 2026

How big is the Italian ecommerce market really?

Different sources publish different numbers, and the gap matters. The most authoritative figure for B2C product purchases comes from the Osservatorio eCommerce B2c Netcomm – Politecnico di Milano (also known as “Polimi”), which valued the Italian B2C ecommerce market at over €62 billion in 2025, growing around 6% year-over-year. The next full-year reading is expected from Politecnico di Milano in spring of next year.

Three commonly cited figures for 2025, side by side:

| Source | 2025 value | Scope | Best used for |

|---|---|---|---|

| Politecnico di Milano / Netcomm | €62B+ | B2C products + services | B2C planning by foreign retailers |

| Casaleggio Associati | €90.6B | Total ecommerce revenue / digital commerce turnover | Total digital commerce universe |

| Statista | ~€52–55B | Physical-goods B2C only | Narrower retail-only view |

The two leading sources don’t actually contradict each other — they measure different things. Politecnico di Milano counts B2C purchases by Italian consumers; Casaleggio Associati counts total ecommerce revenue (B2C + B2B + broader digital commerce turnover). For most retailers shipping physical products to Italian shoppers, the Polimi figure is the one to anchor on: over €40 billion in product purchases plus €22 billion in services like travel and ticketing.

Italy ecommerce statistics: pace, trajectory, and European context

Italy is no longer the breakneck-growth market it was during the pandemic. The product segment grew 6% in 2025, services 8%, and Politecnico di Milano describes the market as consolidating. Casaleggio’s broader-scope total revenue grew 6.1% over the same period — the two methodologies converge on the same growth rate even though absolute values differ.

In Western Europe, Italy still trails the United Kingdom and Germany in internet penetration and ecommerce share of total retail. Italian product ecommerce penetration sits at around 11.2% of total retail, and Italian internet penetration is around 90%. Among large European countries, Italy has the most runway left going into 2026.

Key Point: The deceleration is maturity, not stagnation. Italy is moving from “everyone discovers ecommerce” to “everyone optimizes ecommerce” — and that’s the phase when fulfillment quality, returns handling, and localization start deciding winners.

Who Shops Online in Italy?

Ecommerce in Italy: a digital consumer base of 35 million

35.2 million Italians made at least one online purchase in 2025, per Netcomm — around 60% of the population, with 1.5 million new digital shoppers added year-over-year. Most recent growth is coming from older demographics rather than young adults, who crossed the digital threshold long ago.

Online product purchases now account for 11.2% of total retail spending in Italy, with services online penetration considerably higher. That’s well below the UK or Germany — Italy sits between Western and Southern Europe in digital maturity, with clear convergence room over the forecast period.

The North-South divide is a real planning constraint

Northern regions — Lombardy, Piedmont, Emilia-Romagna, Veneto — generate a disproportionate share of Italian online sales. Milan, Rome, and Naples are the three largest hubs for ecommerce-active companies, with Lombardy, Lazio, and Campania leading by company count.

Southern Italy and the islands, including Sicily, show much lower order density and longer delivery times. For brands, this is a planning factor that affects inventory placement and last-mile cost projections — not just marketing copy.

Features of the Italian Ecommerce Market

Mobile devices now lead basket value

Mobile is the dominant interface for Italian online commerce in 2026, but the picture depends on which metric you look at:

- Mobile commerce payments — Nexi recorded a 61% growth in spending volume on mobile commerce in 2024, with the broader sector growing over 50%.

- Cross-border purchases from smartphones — around 47% of cross-border online orders are placed from a smartphone, per Landmark Global.

- Daily mobile internet use — 84% of Italians aged 18–74 browse via mobile daily, per Casaleggio Associati.

These are different measurements of the same underlying truth: mobile is now the default. Any retailer not optimizing for mobile-first checkout, biometric login, and one-tap payment is leaving conversion on the table.

Cross-border purchases are 39% of online sales

Italians are unusually open to buying from foreign brands. Cross-border online shopping rose from 28.7% of total ecommerce in 2019 to roughly 39% by 2022, and the share has continued upward.

Italians most often shop online cross-border for products that aren’t available locally, with strong demand for fashion from Northern Europe and consumer electronics globally. China remains the largest cross-border source, but EU sellers — especially from Germany, France, and Spain — are gaining ground.

The market in Italy isn’t just an import target. Italian merchants increasingly export through ecommerce platforms to Germany, France, Spain, the UK, and the US, leveraging a strong Made-in-Italy reputation in beauty, fashion, and food. For incoming brands, this shapes the competitive landscape — local sellers are often more digitally sophisticated than headline market research suggests.

Top product categories: where Italian customers spend

Online sales by category in 2025, per Politecnico di Milano:

- Clothing and footwear — top category by online spend, growing in line with the broader market (+5–6%).

- Consumer electronics and IT — the most digitally mature category in Italy, also growing in line with the market.

- Home, garden, and home appliances — growing in line with the broader market.

- Beauty and personal care (Beauty&Pharma) — strongest growth segment in 2025 (+7%), with low online penetration leaving meaningful headroom.

- Food and beverage (Food&Grocery) — also growing at +7%, driven by food delivery and online grocery.

The categories with the lowest online share are also the ones with the most room to grow over the forecast period. For specialized categories like food supplements, category-specific supplements fulfillment infrastructure (batch tracking, expiry-date management, regulated-product handling) becomes a competitive advantage as volumes scale.

What Italian Consumers Expect

Delivery, speed, tracking, and returns

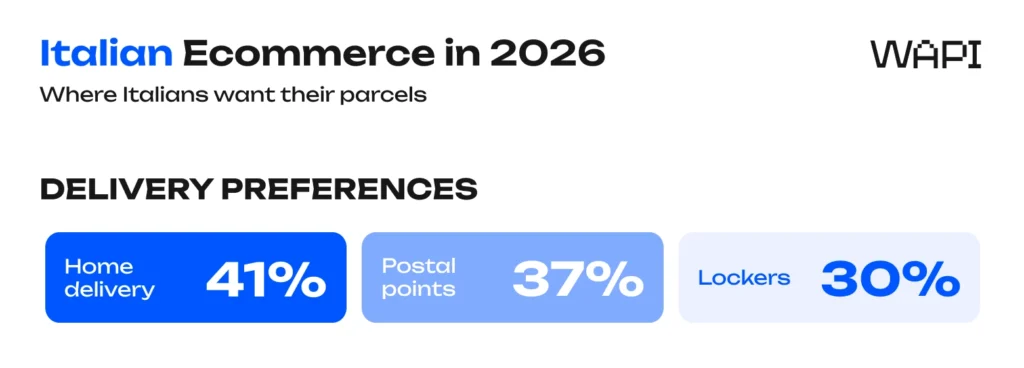

Doorstep home delivery is still the default for 41% of Italian online shoppers, but postal points (37%) and lockers (30%) are rising fast. Out-of-home delivery options that Italian merchants should integrate at checkout:

- Postal points — Poste Italiane network; widely available and the leading PUDO option after home delivery.

- Lockers — InPost passed 3,000 boxes by mid-2025, with strong density around Milan, Turin, and Bologna railway stations. Poste Italiane and DHL are deploying 10,000 automated lockers by 2027.

- BRT and other carriers — most major Italian last-mile carriers now offer locker and parcel-shop options.

- Same-day in major hubs — available in Milan, Rome, and parts of northern Italy via Amazon Prime, Zalando ZEOS, and select grocery players.

Fast delivery is a top-three driver of purchase decisions for Italian online shoppers, cited by around 36% of consumers, alongside product choice and convenience of navigation. The more universal expectation, though, is visibility: roughly 90% of Italians actively track their parcels, and a missed scan event is one of the most common triggers of customer service tickets.

Our advice: Don’t over-promise 24-hour delivery times you can’t consistently hit. Italians value transparency over heroics — accurate ETAs and live tracking events drive higher customer satisfaction than aggressive delivery promises that occasionally slip. A reliable final-mile delivery partner that delivers consistent tracking events matters more than aggressive cutoffs.

Returns are the other margin-killer. Average return rates on Italian fashion ecommerce can exceed 40%, in line with other major European countries. Without a domestic returns address, cross-border sellers face high return-shipping costs and slow inventory recirculation. Local returns infrastructure changes the unit economics meaningfully, especially for fashion and beauty.

Payment Methods Italian Customers Actually Use

The current payment landscape in Italy, by share of online transaction value (NetRetail 2025):

| Method | Share of online value | Notable players | Trend |

|---|---|---|---|

| Digital wallets | ~31% | PayPal, Amazon Pay, Google Pay | Growing |

| Credit cards | ~26% | Visa, Mastercard, Cofidis | Stable |

| Prepaid cards on site | ~24% | PostePay, CartaSi/Bancomat | Stable |

| Bank transfer | ~2% (high-value) | MyBank, SEPA Instant | Growing slowly |

| Cash on delivery / pay-on-use | ~11% (incl. ~1.2% cash) | Multi-carrier | Stable in selective categories |

| Buy Now Pay Later (BNPL) | <7% but fast-growing | Scalapay, Klarna | Strong growth |

Two methodology notes worth understanding: NetRetail’s 11% figure for “pay at delivery or service usage” combines cash-on-delivery (around 1.2%) with other deferred-payment methods. Other industry sources that report COD shares of 4% or lower are measuring true cash-only COD. The methodologies differ — but cash COD remains a meaningful payment option in specific categories and demographic segments, especially in southern regions and for first-time online buyers.

PayPal alone is the first-choice method for around 39% of Italians shopping online, a level of dominance that doesn’t exist in most other European countries. PostePay — Poste Italiane’s prepaid card — is widely used by younger consumers and the unbanked, and should be supported by any merchant treating Italy as a serious target.

A practical Italian payment lineup in 2026 should include:

- PayPal (essential — the first-choice method for ~39% of Italian online consumers)

- Credit and debit cards with explicit PostePay support

- SEPA bank transfer or MyBank for higher-value B2B-style purchases

- BNPL via Scalapay or Klarna for fashion, beauty, and electronics baskets

- Cash on delivery as an optional fallback for selective categories: makeup, skincare, food supplements

Insight: In Italy, COD works best as a strategic option for trust-sensitive categories — beauty, supplements, electronics — and for reaching older demographics or southern regions where cash-at-delivery still drives meaningful conversion. For sellers scaling further into Central and Eastern Europe, COD remains a leading payment method in many markets, and it’s worth setting it up once with a logistics partner that supports it across the broader region.

Italian Logistics Realities

Last-mile costs are climbing

Average Italian last-mile costs have grown from roughly €8 to €11 per shipment in recent years, with delivery surcharges of up to €8 per parcel in difficult zones.

For cross-border sellers shipping into Italy from a German or Dutch warehouse, those costs stack on top of customs handling and longer transit times — eroding the margin that justified cross-border in the first place. Brands that anchor inventory inside Italy typically see materially better delivery times and unit economics once volume is steady.

The southern gap and the locker fix

Delivery density in Calabria, Sicily, and parts of Apulia remains roughly 30% below the northern average. New Poste Italiane and DHL hubs in Naples and Palermo are narrowing the gap, but cross-border merchants relying solely on a Milan or Bologna depot will still see slower delivery times and higher failure rates south of Rome.

PUDO points and lockers reduce failed deliveries dramatically and lower per-parcel last-mile costs. They also align with the rising share of Italians (around 30%) who now prefer locker pickup over home delivery. Integrating with Poste Italiane, InPost, and BRT locker networks at checkout typically delivers a measurable lift in completed orders.

What to Set Up Before Shipping to Italy

Before launching or scaling into Italy, cross-border brands should have these five blocks in place:

- Carrier mix — at least one home-delivery carrier plus integration with parcel shops and lockers (Poste Italiane, InPost, BRT). Single-carrier setups underperform consistently.

- Returns setup — a local or regional returns address, fast inspection workflow, and inventory recirculation. Without this, fashion and beauty unit economics break above modest volumes.

- Payment setup — PayPal, cards with PostePay support, BNPL for fashion/beauty/electronics, and selective COD for categories where it still moves the needle.

- Inventory threshold — a clear trigger for when pan-EU fulfillment is enough and when a dedicated Italy flow makes sense (see next section).

- Category specifics — fashion returns workflows, cosmetics handling (batch tracking, expiry, restricted shipping), supplements documentation (notifications to the Italian Ministry of Health, batch/lot traceability).

The brands that ship into Italy without ticking these boxes typically see returns build up at a foreign warehouse, conversion drop on payment screens that don’t match local habits, and customer service tickets escalate over delivery transparency — all things that don’t show up in a market-size report.

How Cross-Border Sellers Should Approach the Italian Market

Local fulfillment beats pan-EU once volume is real

For low-volume tests, pan-EU fulfillment from Germany or the Netherlands works fine. Once Italian order volume crosses a few hundred parcels per week, the math flips toward dedicated Italian fulfillment: faster delivery times, lower last-mile costs, and easier returns.

A €3 saving per parcel on 500 parcels a week is roughly €78,000 a year — enough to fund the full local fulfillment switch and still come out ahead.

5 signs it’s time to move inventory into Italy:

- Italian order volume sustains 300+ parcels per week for two consecutive months

- Return rate exceeds 25%, especially in fashion or beauty

- Customer service tickets spike on transit-time and tracking complaints

- Paid acquisition efficiency drops because conversion is bottlenecked by the delivery promise

- Customs and duty handling on cross-border shipments is materially eroding margin per order

Localize beyond translation, layer marketplaces with DTC

Italian-language product pages, Italian customer service, and Italian-language returns instructions are minimum table stakes. Real localization means matching local payment habits, pricing in euros with VAT included, and aligning delivery promises with what local competition offers — not just selling products online through a translated template.

Amazon, eBay, and Zalando are the dominant online platforms by traffic in Italy. The most resilient cross-border strategies layer marketplaces — for discovery and trust — on top of a localized DTC website for margin and customer data.

Selling exclusively on marketplaces leaves the brand exposed to algorithm changes and increasing competition. Selling exclusively DTC means slow, expensive customer acquisition. The hybrid approach is the practical winning model in Italy right now.

Final Take: Italy Is a Logistics Game

Italian ecommerce isn’t growing at pandemic-era speed anymore, but going into 2026 it remains one of the most underexploited large markets in Western Europe for cross-border sellers willing to build proper local infrastructure.

Steady growth, a 35-million digital consumer base, a 39% cross-border share, and clear preference for transparent fast delivery — those are not the conditions for a passive market entry.

Our Advice: Treat Italy as a logistics-first market, not a marketing-first one. The brands that win Italian customers in 2026 and beyond will be the ones whose Italian fulfillment, payment mix, and returns experience match the bar set by Amazon and the strongest domestic retailers — not the ones who simply translated the checkout page.

FAQ: Frequently Asked Questions

How big is the Italian ecommerce market?

Italian B2C ecommerce reached over €62 billion in 2025 (Politecnico di Milano / Netcomm), growing around 6% year-over-year. The broader Casaleggio Associati estimate, which includes B2B and total digital commerce revenue, puts the market at €90.6 billion with 6.1% growth — the two figures measure different scopes but converge on the same growth rate.

Is Italy a good market for cross-border ecommerce?

Yes — and increasingly so. About 39% of Italian online sales are already cross-border, Italians actively seek products not available locally, and product ecommerce penetration is still around 11.2% of total retail. The catch is logistics: cross-border sellers without local Italian fulfillment face higher last-mile costs and slower delivery times that hurt conversion.

What is the most popular online payment method in Italy?

Digital wallets are now the leading method at around 31% of online value, with PayPal as the dominant single method — the first choice for roughly 39% of Italian online consumers. Credit cards (Visa, Mastercard) follow at around 26%, and prepaid cards on site (PostePay, CartaSi/Bancomat) at around 24%.

How fast do Italian shoppers expect delivery?

Around 36% of Italian consumers cite fast delivery as a top-three driver of their purchase decision — but the more universal expectation is delivery transparency. Roughly 90% of Italian shoppers actively track their parcels, so accurate ETAs and live tracking events drive higher customer satisfaction than aggressive 24-hour delivery promises that occasionally slip.

Should I use a local fulfillment warehouse in Italy?

For volumes under a few hundred parcels per week, pan-EU fulfillment from Germany or the Netherlands is usually sufficient. Above 300+ parcels per week consistently, local Italian fulfillment typically pays for itself through lower last-mile costs, faster delivery times, and meaningfully better returns handling — especially for fashion and beauty categories where return rates can exceed 40%.

How does cash on delivery in Italy work for cross-border sellers?

Cash on delivery in Italy, known locally as contrassegno, is a selective rather than mainstream payment method — strongest in beauty, supplements, and electronics, in southern regions, and with first-time buyers who want to pay only once the parcel is in hand. Offered well, it lifts conversion in exactly the segments that are hardest to win on card alone. The operational catch is that COD only pays off when most parcels are accepted and paid for on delivery. WAPI runs cash on delivery in Italy end to end — Italian-language delivery notifications, two delivery attempts before return, and weekly payouts in EUR — at a buyout rate around 79% on disciplined COD traffic. That keeps cash on delivery in Italy a margin-positive option rather than a refusal-and-returns liability.

Does WAPI have a fulfillment warehouse in Italy?

Yes. WAPI operates a fulfillment warehouse in Italy, located in Rimini, that holds stock inside the country and ships domestic Italian orders in 24 to 48 hours. For the cross-border sellers this guide is aimed at, a local Italian warehouse does two things at once: it removes the cross-border step and customs handling that inflate last-mile cost and transit time, and it makes cash on delivery in Italy practical to offer, since parcels ship same-country instead of routing in from Germany or the Netherlands. It is the same “local fulfillment beats pan-EU once volume is real” logic from the section above, with an address attached.

Sources and References

- Osservatorio eCommerce B2c Netcomm – Politecnico di Milano (2025) — L’eCommerce B2c in Italia supererà i 62 miliardi di € nel 2025 (+6%), con 35,2 milioni di Consumatori Online — consorzionetcomm.it

- NetRetail 2025 — annual study on Italian online buying behavior, by Netcomm in collaboration with BRT, Confcommercio, Publitalia ’80, Magnews, Oney, and Banca Sella.

- Casaleggio Associati — Ecommerce Italy 2026 Report — total Italian ecommerce revenue estimated at €90.6B in 2025, +6.1% YoY — ecommerceitalia.info

- Cross-Border Magazine (2025) — E-commerce Payments Italy 2025 — payment landscape overview — cross-border-magazine.com

- Worldometer / IMF (2025) — Europe GDP rankings — worldometers.info

- Landmark Global — cross-border smartphone purchase share data

- Nexi / Politecnico di Milano — mobile payment growth data (+61% spending volume on mobile commerce in 2024)

Keep in touch with WAPI!

Get free ecommerce tips, news, webinars and other stuff.