The European E-commerce Report 2025 ranks Spain third in Europe for B2C ecommerce, ahead of Germany on the report’s 2024 methodology. Most cross-border brands haven’t caught up to that yet. They still build their EU rollout starting with Germany, then France, then Italy or Poland, and treat Spain as something to plug in later through a pan-EU warehouse.

That order of operations made sense five years ago. It doesn’t anymore.

Spanish ecommerce closed 2024 at €95.2 billion in CNMC turnover. Mobile drives 71% of transactions. More than half of every euro Spanish shoppers spend online still goes to a foreign merchant before the parcel reaches a Spanish doorstep. That last number is the one that should reorder the priority list for any brand planning European expansion in 2026.

What follows is the practical view: market size, who’s buying, the payment habits that look strange if you’ve only built for Northern Europe, and the logistics that quietly decide whether your cross-border launch clears margin or eats it.

Spanish Ecommerce Market: Size and Growth Heading into 2026

How big is the Spanish ecommerce market really?

This is the section where sources disagree and the disagreement actually matters for planning. Anchor on CNMC. The national markets and competition commission publishes quarterly, sits inside the regulator, and is the figure local trade press uses. CNMC put 2024 at €95.2 billion in total ecommerce turnover, up 13.1% year on year, with 1.8 billion transactions across the calendar year.

The latest quarterly read points in the same direction. Q3 2025 hit €29.3 billion in three months, up 19.3% year on year, with more than 508 million transactions. If that trajectory holds, full-year 2025 is heading toward €115 billion — a number Spanish trade press is already openly modeling.

Three figures you’ll see thrown around for the same market:

| Source | Headline figure | Scope | Best used for |

| CNMC | €95.2B (2024) | Total turnover (goods + services, B2C + cross-border) | Anchoring the headline and local conversations |

| ResearchAndMarkets / IMARC | ~$88B | B2C ecommerce GMV | B2C-only planning |

| Mordor Intelligence | 84.97% | B2C share of 2025 ecommerce value | Channel mix |

CNMC is the right anchor for top-line numbers. The B2C subset sits around $88B in 2025 and is forecast to hit $121B by 2029. High single-digit to low double-digit growth, with no obvious cooling.

Spain ecommerce statistics: pace, trajectory, and European context

Spain has outgrown the European average for three years running. Southern Europe grew 9% in 2024. Western Europe grew 6%. Spain grew 13%, and Q3 2025 came in at +19%. The drivers are the boring ones: late maturity catching up, mobile-native adoption, and a Latin American export tailwind that doesn’t exist in any other large European market.

Key Point: Treating Spain as a “secondary Southern European market” is a 2020 reflex. In the most recent European B2C rankings (methodology depending), Spain sits ahead of Germany and grows at roughly twice the EU average. For anyone prioritizing European launches in 2026, the case is stronger than it has been in a decade.

Who Shops Online in Spain?

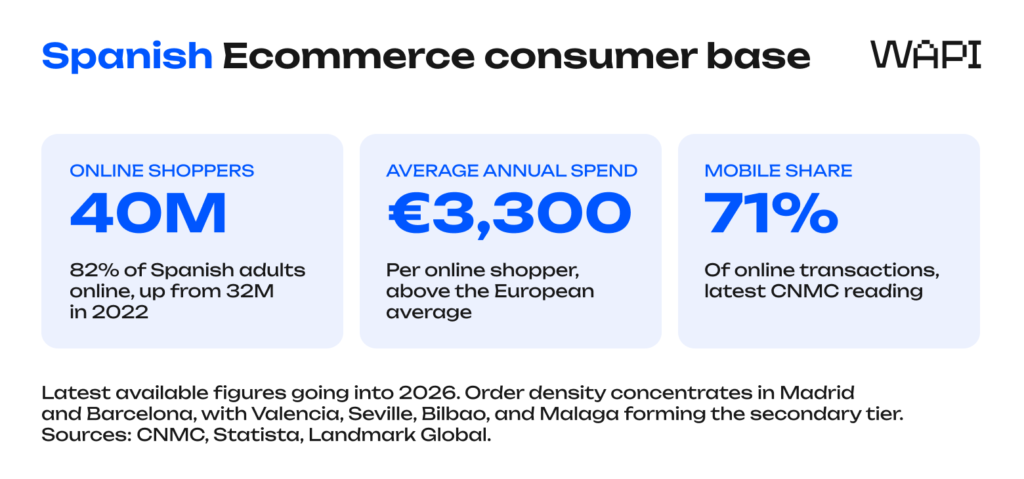

Spanish ecommerce: a digital consumer base of 40 million

Roughly 40 million Spaniards bought something online in 2025, up from 32 million in 2022 — about 82% of the adult population. Most of the new growth isn’t coming from digital natives; they crossed that line years ago. It’s coming from older shoppers and rural areas, helped by the 5G rollout that now reaches 96% of urban regions and Kit Digital vouchers that pushed tens of thousands of small Spanish merchants online in the last two years. Demand is widening at the same time supply is thickening.

The average Spanish online shopper spends around €3,300 a year. That’s well above the European average and still rising.

The Madrid–Barcelona axis and the regional gap

Order density is concentrated. Madrid and Barcelona together generate a disproportionate share of Spanish ecommerce volume — both as origin (most merchants and platforms sit there) and as destination (most parcels land there). Valencia, Seville, Bilbao, and Malaga form the secondary tier and behave like the top two on conversion and delivery time.

Rural Spain, the Canary Islands, Ceuta, and Melilla are a different planning problem. Last-mile times run longer, per-parcel costs run higher, and the tax map splits there: mainland Spain and the Balearic Islands sit inside the standard Spanish/EU VAT framework, the Canary Islands use IGIC instead of VAT (still inside the EU customs territory but outside the VAT area), and Ceuta and Melilla sit outside both the EU customs union and the VAT area, with IPSI as the local indirect tax. A one-rate-fits-all shipping setup quietly loses money on those flows.

Features of the Spanish Ecommerce Market

Mobile dominates, and the gap is still widening

Mobile is the default in Spanish ecommerce. The percentages depend on what you measure:

- Smartphone share of B2C traffic — 69.7% in 2025 (Mordor Intelligence).

- Mobile share of total transactions — 71% in Q1 2025 (CNMC-linked sector data).

- Smartphone share of completed purchases — 51% (Statista).

Pick whichever you like. The conclusion is the same. A checkout that needs a desktop or a two-handed keyboard to complete is bleeding conversion in Spain. One-tap payment, biometric login, and a basket that survives a single-thumb interaction are the floor, not the ceiling.

Cross-border purchases dominate Spanish online spending

This is the headline feature of the Spanish market and the one I’d reread before anything else if I were planning a launch.

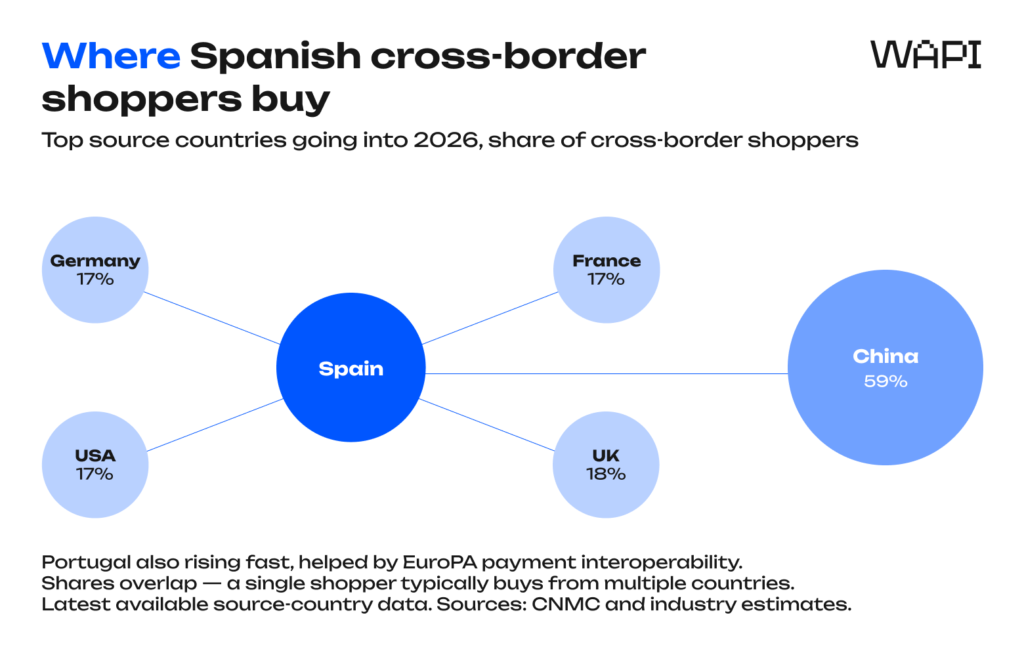

More than half of Spanish ecommerce spending leaves the country. CNMC Q3 2025 puts the share at 53.4% by revenue and 63.1% by transaction count. Full-year 2024 sat higher at 61.5% by revenue. The number moves quarter to quarter, but the direction is consistent: Spanish shoppers buy abroad more than shoppers in almost any other major European market.

Where the money goes:

- China — about 59% of Spanish cross-border spend (Shein, AliExpress, Temu)

- Germany, France, USA, UK — roughly 17–18% each

- Portugal — rising fast, helped by EuroPA payment interoperability

Two practical reads. First, you don’t need a Spanish domain to sell to Spaniards. The cross-border habit is already there. Second, you’re not competing with Spanish retailers alone; you’re competing with the full global cross-border field. Pricing and shipping economics need to be benchmarked against Shein and Amazon, not just against El Corte Inglés.

There’s an export angle most foreign brands underestimate. Spanish-headquartered retailers (Inditex, Mango, El Corte Inglés, plus the marketplace tier) have built genuinely sophisticated cross-border flows into Latin America on the back of Spanish-language and euro pricing. That’s a competitive set you don’t see if you only look at the EU map.

Top product categories: where Spanish customers spend

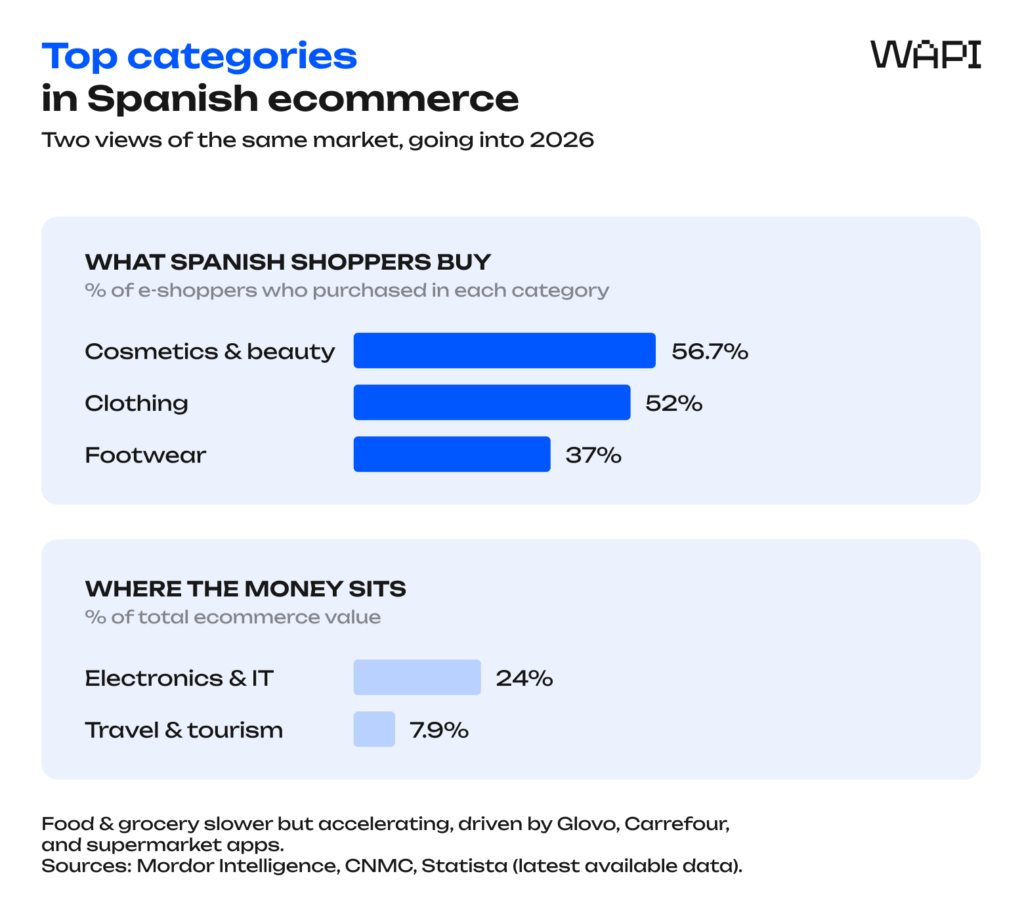

The biggest categories by online sales in 2025:

- Consumer electronics and IT — 24% of total ecommerce value, the single largest category.

- Fashion and footwear — historically dominant and still close to the top. 52% of Spanish consumers buy clothing online; 37% buy shoes.

- Travel and tourism — 7.9% of total online turnover, the biggest single services vertical and a large share of overall ecommerce because of how Spain measures it.

- Beauty and personal care — strong cross-border pull. 56.7% of Spanish e-shoppers purchase cosmetics online.

- Food and grocery — slower but accelerating, driven by Glovo, Carrefour, and supermarket apps.

For specialized categories like supplements, sport nutrition, and cosmetics, category-specific handling (batch tracking, expiry-date control, regulated-product paperwork) turns into a real advantage past a few hundred parcels a week. The brands that figure this out early stop competing on price and start competing on reliability.

What Spanish Consumers Expect

Delivery, speed, tracking, returns

Free shipping is the single biggest driver of store choice for Spanish shoppers, cited by around 65%. Fast delivery comes second at 33%, then product availability at 31%. Cart abandonment sits at a stubborn 73.5–74%, and the leading trigger isn’t price or stock. It’s delivery cost that doesn’t show up until the last screen. 62% of Spanish consumers say they want shipping cost visible from the product page.

Out-of-home delivery is no longer a fringe option. The networks worth integrating at checkout:

- Correos CityPaq — over 4,200 lockers nationwide, run by the national postal operator. The default option for rural Spain and the islands.

- InPost — nearly 4,000 lockers across the Iberian Peninsula by end of 2025, with 99% accessible six days a week. InPost bought Sending in 2025 to bolt nationwide door delivery onto its locker network.

- DHL and CTT Express — joint Iberian B2C network with locker integration.

- Same-day in major hubs — Madrid, Barcelona, Valencia, Bilbao, Seville, Malaga, via Amazon Prime, Glovo grocery, and El Corte Inglés’s two-hour Click & Express service.

Our advice: Don’t try to win the basket by burying shipping costs. Spanish shoppers want the number visible early. They’d rather pay a transparent €4 than discover a €4 surcharge on the final screen. A reliable final-mile delivery partner that hits its tracking events on time matters more than an aggressive same-day promise that occasionally slips. Predictability beats heroics.

Returns are the second margin question. Spanish fashion returns run around 25–35% on apparel, lower on footwear and accessories, in line with other Southern European markets. Without a local return address, you either absorb the inbound shipping cost or push it onto the customer and watch conversion drop. For fashion, beauty, and electronics, a domestic returns flow isn’t an optimization. It’s the line between a viable Spanish P&L and a leaky one.

Payment Methods Spanish Customers Actually Use

The payment mix in Spain is best read as a set of source-dependent signals rather than a clean 100% split:

| Method | Approx. reported share / signal | Notable players | Trend |

| Credit and debit cards | ~44% | Visa, Mastercard, Redsys | Declining slowly |

| Digital wallets | ~31% | PayPal, Bizum, Apple Pay, Google Pay | Growing fast |

| Bank transfer / A2A | ~21% | Bizum, SEPA Instant | Growing fast |

| BNPL | ~7%, accelerating | Klarna, SeQura, Aplazame, Afterpay | Strong growth |

| Cash on delivery | <2% | Multi-carrier | Stable in selective categories |

Two methodology notes before the practical advice. Bizum sits across two buckets: some sources file it as a digital wallet, others as account-to-account. It doesn’t really matter which label you pick. What matters is that it’s the most important Spanish payment innovation of the last decade. Second, PayPal’s role in Spain is unusual by European standards: roughly 80% user recognition and consistent top placement in surveys of preferred online payment methods.

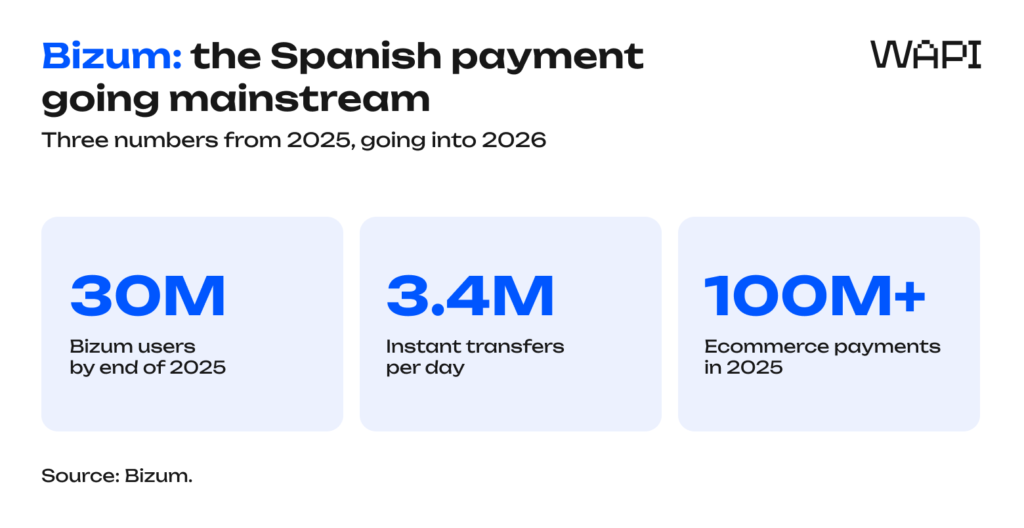

Bizum: the Spanish payment no foreign retailer can ignore

Bizum reached 30 million users in 2025, processed 3.4 million instant transfers a day, and closed the year with more than 100 million ecommerce payments on its rails. Its in-store rollout began on 18 May 2026 but stayed deliberately small at launch: only CaixaBank, Sabadell, and Bankinter customers in the first wave, with the standalone Bizum Pay wallet app pushed back to June. Mass adoption is the September–October story, not the May story.

For ecommerce sellers, the in-store timeline matters less than the online one. Bizum at checkout has been around since 2019, and it consistently lowers cart abandonment compared to card-only flows. If your audience is mainstream Spanish consumers (especially mobile-first ones), Bizum belongs in the checkout. If you skew older or tourist-adjacent, PayPal still carries more weight. Most serious Spanish online stores now show both.

A practical Spanish payment lineup in 2026:

- Credit and debit cards with strong 3DS support — still the backbone at roughly 44% of value

- PayPal — non-negotiable; the most-recognized wallet in Spain

- Bizum — non-negotiable for domestic baskets, particularly mobile and under-40

- BNPL via Klarna, SeQura, or Aplazame for fashion, electronics, and lifestyle

- SEPA Instant for higher-ticket and B2B-adjacent purchases

- Cash on delivery only where the category and demographic actually pull on it (useful in narrow segments)

Insight: Cards still carry the most online value in Spain, but the growth is all coming from wallets and instant A2A. A checkout running cards + PayPal + Bizum covers the dominant card, wallet, and instant-payment expectations in Spain before you add anything else. For brands eyeing the Iberian–Latin American corridor, the same rails reach the largest Spanish-speaking segments abroad.

Spanish Logistics Realities

Last-mile costs and the cross-border math

Mainland Spanish last-mile is competitive. The Madrid–Barcelona–Valencia–Bilbao corridor is well served by Correos, SEUR, MRW, GLS, InPost, and DHL, and rates are roughly in line with France. The Canary Islands, Ceuta, and Melilla are the exception: different VAT regimes (and, in Ceuta and Melilla, different customs status) add paperwork and cost on every parcel headed there.

If you’re shipping into mainland Spain from a German or French warehouse, the extra cost usually comes from longer linehaul, less flexible carrier handoffs, and slower returns recirculation rather than customs. Customs and tax handling become a separate issue for the Canary Islands, Ceuta, and Melilla. The margin that justified the cross-border setup starts disappearing. Brands that anchor inventory inside Spain typically see materially better delivery times and unit economics once weekly volume stabilizes (usually somewhere north of a few hundred parcels per week).

Lockers reshaped the last mile faster than anyone expected

Lockers are mainstream in Spain now. Between Correos CityPaq (4,200+ terminals) and InPost (nearly 4,000 across Iberia), the network reaches the suburbs of every major metro and most secondary cities. Failed first-attempt home delivery still hovers near 25% in dense urban areas. Lockers eliminate most of that. They also cut last-mile CO₂ emissions by 13–32% versus standard home delivery, per recent European studies, which is becoming a real consideration as more brands report on Scope 3.

Plugging Correos CityPaq and InPost into your checkout typically lifts completed orders by a measurable margin and lowers re-delivery costs. Spanish consumers stopped treating lockers as a downgrade about two years ago.

What to Set Up Before Shipping to Spain

Five blocks worth having in place before you scale into Spain:

- Carrier mix — at least one home-delivery carrier (Correos, SEUR, GLS, or DHL) plus locker integration via Correos CityPaq and InPost. Single-carrier setups underperform consistently.

- Returns setup — a local or regional return address, fast inspection workflow, and inventory recirculation. Without it, fashion and beauty break above modest volumes.

- Payment setup — cards + PayPal + Bizum at minimum, BNPL for relevant categories, SEPA Instant for higher-ticket items.

- Inventory threshold — a defined trigger for when pan-EU fulfillment is enough and when you flip into a dedicated Spanish flow (covered below).

- Category specifics — fashion returns workflow, cosmetics handling (batch tracking, expiry, restricted shipping), food supplement notification to the competent Spanish authority or AESAN where applicable, Spanish-language label checks, batch traceability, and GDPR-compliant customer data management.

Skipping any of these usually shows up the same way: returns building up at a foreign warehouse, conversion sliding on payment screens that don’t match local habits, support tickets stacking up over delivery transparency. None of those problems make it into a market-sizing report, which is exactly why they catch teams off guard six months into a launch.

How Cross-Border Sellers Should Approach the Spanish Market

Local fulfillment beats pan-EU once volume is real

For low-volume tests, a German or French warehouse handles Spain fine. Past a few hundred parcels a week, the math flips toward dedicated Spanish fulfillment: faster delivery, lower last-mile cost, and a domestic returns address that changes the fashion and beauty P&L outright. The question for most cross-border brands isn’t whether to set up ecommerce fulfillment in Spain. It’s when.

A €3 saving per parcel on 500 parcels a week is roughly €78,000 a year. That’s the full local fulfillment switch funded with margin to spare.

5 signs it’s time to move inventory into Spain:

- Spanish order volume holds at 300+ parcels per week for two consecutive months

- Return rate clears 25%, particularly in fashion or beauty

- Customer service tickets spike on transit-time and tracking complaints

- Paid acquisition efficiency drops because conversion is bottlenecked on delivery promise

- Special-zone handling for the Canary Islands, Ceuta, or Melilla is visibly eroding margin per order

Localize beyond translation, and layer marketplaces with DTC

Spanish-language product pages, Spanish customer service, and Spanish-language return instructions are table stakes. Real localization means matching local payment habits, pricing in euros with VAT included, showing shipping costs from the product page, and pacing delivery promises against the local competition. Sticking a translated template on top of an English store and calling it a market entry doesn’t qualify.

Amazon, AliExpress, El Corte Inglés, Carrefour, Miravia, PcComponentes, Fnac, and Zalando dominate Spanish online traffic. Each does a different job: Amazon for breadth, El Corte Inglés for premium fashion and trust, PcComponentes for electronics, Miravia for discovery shopping. The resilient strategies layer marketplaces (for discovery and trust) on top of a localized DTC site (for margin and customer data).

Going marketplace-only leaves you exposed to algorithm changes and rising fees. Going DTC-only means slow, expensive customer acquisition in a market where 75% of online buyers already shop on major marketplaces. The hybrid model wins in Spain right now, and it’s likely to keep winning through 2026.

Final Take: Spain Is Becoming Europe’s Cross-Border Test Market

Spanish ecommerce has climbed into the top tier of European B2C markets, posts double the European growth rate, and shows where checkout expectations are moving: Bizum, mobile-first flows, and instant-payment habits. None of that supports treating Spain as a pan-EU afterthought going into 2026.

40 million online shoppers. A cross-border channel that consistently captures more than half of online spending. 71% of transactions on mobile. An out-of-home delivery network that already rivals Northern European density. That’s not a passive market-entry profile. It’s a market that rewards committed setups: proper Spain ecommerce fulfillment, a checkout localized down to the wallet preference, a returns flow on Spanish soil. Cross-border fulfillment in Spain has shifted from optional to table stakes in roughly three years. 2026 is the year that gap starts showing up in everyone else’s numbers.

FAQ

Do I need a Spanish legal entity to sell ecommerce in Spain?

No, not for most cross-border setups. EU sellers can ship into Spain under standard OSS VAT registrations from their home country. Non-EU sellers usually appoint a fiscal representative or use IOSS for consumer parcels under €150. A Spanish entity helps if you’re hiring locally, opening a Spanish bank account, or running paid acquisition with Spanish billing. For most ecommerce brands launching into Spain in 2026, none of those are required upfront.

How should I handle VAT for cross-border Spanish ecommerce sales?

EU sellers should use the One-Stop Shop (OSS) to declare Spanish VAT centrally through their home tax authority — no separate Spanish VAT registration required. Non-EU sellers shipping consumer parcels under €150 should use the Import One-Stop Shop (IOSS), which lets you collect VAT at checkout instead of letting it surprise the customer at delivery. Parcels over €150, or anything destined for the Canary Islands, Ceuta, or Melilla, sit outside the OSS/IOSS framework and need separate handling.

Does WAPI offer cash on delivery in Spain?

Yes. Cash on delivery in Spain is one of WAPI’s core capabilities. We run cash on delivery across 19 European markets, and Spain consistently sits in the top tier on buyout rates — around 80% on disciplined operations. Our Spanish hub also covers Portugal cross-border. The commercial model is margin-based with weekly EUR payouts, and the operational differentiator is real-time webhook signals fired to the client’s call center on every trouble status (failed delivery, unreachable customer, refused at the door). In practice, brands running this setup typically see buyout rates 10–15 percentage points above ship-and-hope alternatives.

What does WAPI’s warehousing and fulfillment in Spain include?

WAPI runs multiple warehouses in Spain with 24–48 hour delivery within the country and 2–3 day shipping across the EU. The full setup covers picking, packing, label-and-ship, returns processing, real-time inventory dashboards, and out-of-the-box integration with Shopify, WooCommerce, eBay, BigCommerce, and Amazon (including FBA prep and FBM). Categories handled include supplements, cosmetics and beauty, electronics, household goods, and apparel. For supplements specifically, the Spanish warehouse runs the AESAN food-supplement notification protocol before products go on the shelf, which most cross-border 3PLs leave to the brand.

How long does it take to launch Spanish ecommerce fulfillment with a 3PL?

Anywhere from 48 hours to two weeks, and the variance is almost entirely on the client side. Brands arriving with clean SKU data, ready packaging specs, and a defined returns policy can be live within 2-3 business days. Brands still finalizing compliance paperwork — particularly for supplements — or working through carrier integration take longer. The warehouse side is rarely the bottleneck.

Keep in touch with WAPI!

Get free ecommerce tips, news, webinars and other stuff.